Articles & Posts

-

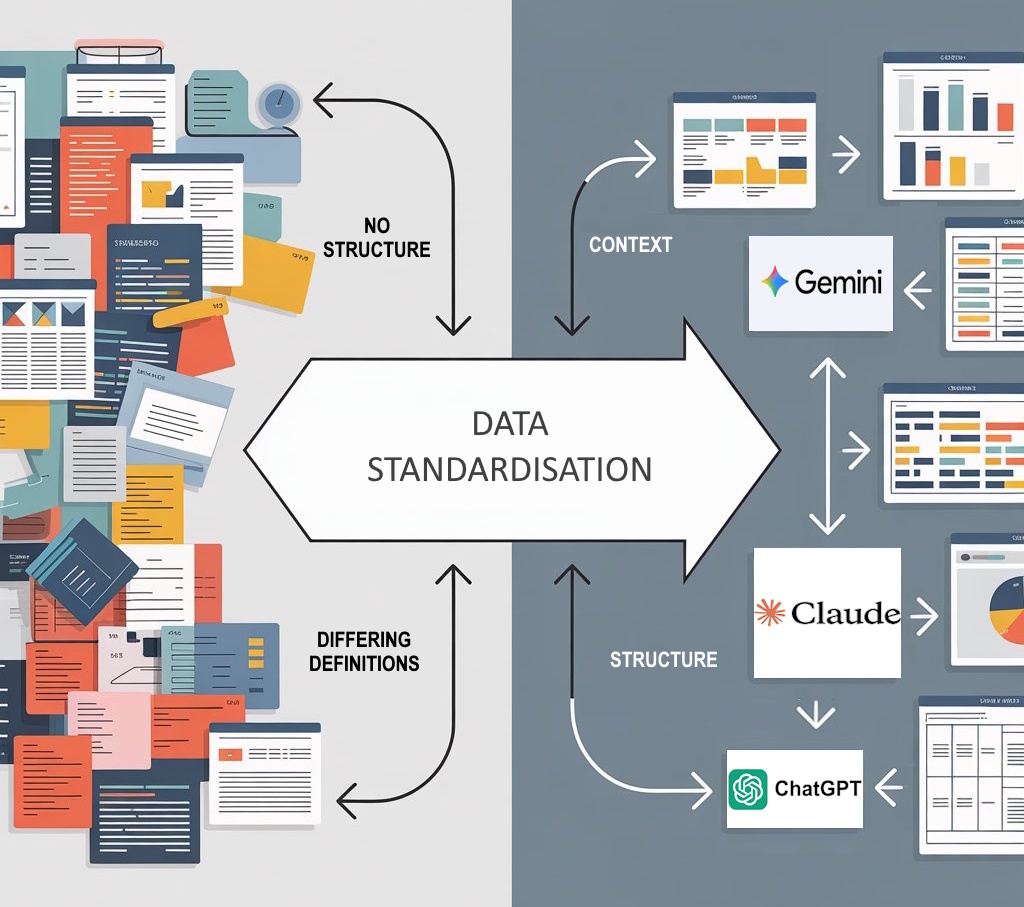

Why AI Demands Investment in Public Data Infrastructure and XBRL

When an AI chatbot tells an investor that revenue jumped 40%, but instead it fell, the issue probably isn’t the AI model, it’s most likely the fragmented, inconsistent, and poorly structured data it’s finding on the internet. Public datasets need to be “AI-ready”: structured with clear definitions, validated for quality, and enriched with semantic metadata that helps AI understand context. Standards like XBRL already provide this foundation for financial reporting, but they need modernising to become the semantic layer that AI systems require. The choice is stark: build proper data infrastructure now, or watch AI confidently mislead decision-makers at scale.

-

Digital First is Here

The encouraging news, as I predicted in an earlier article, is that a healthy number of European vendors now offer Digital First reporting capabilities; that is the sweet spot where well-formed HTML meets XBRL tags. While many are just starting their journeys, they already serve clients for ESEF, CSRD, and local reporting needs. This article shares the key findings of a recent survey. It identifies the traits common to this new generation of tools, and what’s needed to evolve from basic digital-first tagging to fully integrated corporate reporting.

-

The Potential of XBRL as a Semantic Layer

Enterprises are increasingly adopting cloud-native platforms, data lakes, lakehouses, and mesh networks to transform raw business data into actionable insights. A key component in these modern architectures is the semantic layer, which makes complex data understandable to humans. In regulatory and digital reporting, XBRL is the pivotal standard, providing precisely this kind of semantic structure. This article explores how XBRL can function within today’s modern data frameworks, and how it can help create a richer, more intelligent ecosystem for business information.

-

Digital Reporting and XBRL Multi Target Documents

The UK Financial Reporting Council’s UKSEF framework combines multiple XBRL taxonomies using a rare approach – Multi Target Document (MTD). This unusual choice appears to create headaches for software vendors and data analysts, pushing problems down the supply chain instead of solving them with a single base taxonomy, as normal. In this article, I explore why designers might choose MTD, its real benefits, when it works, and when it doesn’t by drawing on insights from practitioners across the field.

-

Digital Financial Reporting and AI

The question ‘Is Automatic XBRL Tagging Feasible Using AI and LLM systems’ is now common at XBRL conferences. Research suggests LLM systems achieve 79% accuracy when reading annual reports. However, XII research shows that using semantic tags from XBRL reports produces better results and the data provides significant benefits to deeper analysis. Reversing the process, this article asks if AI can tag a financial report with XBRL? Based upon our own testing and that of others we find that AI understanding is not quite there yet and needs augmentation (RAG). As always, the answer for AI is in the future.

-

What links Datapoints, Label Encoding, XBRL, and AI?

The notion that abstract encoding is bad for Large Language Models (LLMs), leads to the assumption that it must be unhelpful for human understanding. Generating encoded labels for various IT applications is essential, however it introduces special challenges for how XBRL collection systems operate. Evaluating the impact of the abstract encoding on the 27 European country authorities that collect and validate the XBRL and the thousands of banks that submit them is important in terms of the effects on the costs of regulatory reporting. This article also reviews if DPM encoding also acts as a barrier to using advanced AI…

-

Integrated Digital Financial Reporting

Digital Financial Reporting is moving to a new phase of development. The move towards standardisation using Inline XBRL (HTML with XBRL tags) are multiple. Limitations with tagging the old PDF-files, means that a new ‘digital-first’ approach is emerging using HTML-based content management systems. An approach which offers many process advantages. This will impact the 50,000 that will need to provide their annual report, according to the ESEF guidelines and their sustainability report under Europe’s CSRD initiatives. This article explores this further.

-

Digital Financial Reporting

Digital Financial Reporting is the new phrase for UK and European accountants, auditors, and IT departments to come to terms with, but what does it really mean? ESEF and UKSEF has required digital reports for three years and around 5,000 companies to submit them. The next step for Sustainability reports to be prepared and submitted in the same way. This paper tries to analyse the progress and attempts to look further into the future to see how we can improve the experience.

-

Improving XBRL for Data Modelling

There is a fundamental conflict between the modelling approaches of XBRL and the Data Point Methodology (DPM). The EBA and EIOPA use both. This raises the questions of they use both, is there a weakness in one of the approaches, or is it just a lack of understanding. Reviewing the key requirements of large reporting frameworks, like those for EBA CRD and EIOPA Solvency, this paper assesses the status of XBRL specifications to meet them and to enable XBRL to provide master data management capabilities for reporting frameworks.